Mortgage Backed Securities Default Rate

Mortgage Backed Securities Held By The Federal Reserve All Maturities Discontinued Mbst Fred St Louis Fed

Mall And Hotel Loans Are Blowing Up Commercial Mortgage Backed Securities Finanz Dk

Which U S Bank Is The Largest Holder Of Mortgage Backed Securities

Residential Mortgage Backed Securities And The To Be Announced Tba Market

Rmbs Issuance In The U S 2019 Statista

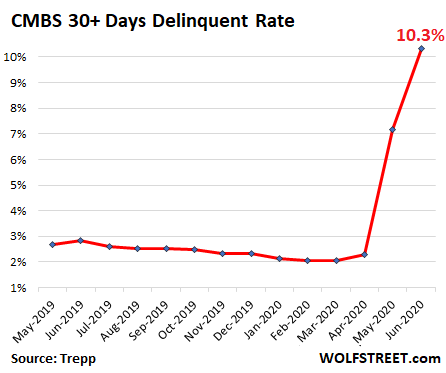

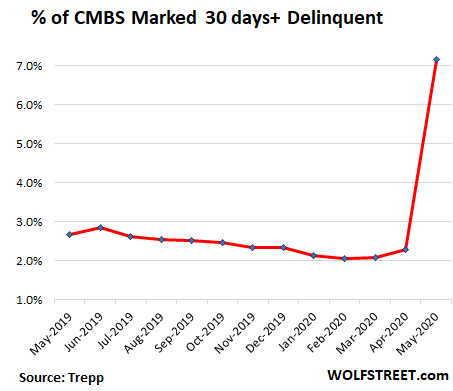

Cmbs Delinquency Rate Spikes By Most On Record Finanz Dk

:max_bytes(150000):strip_icc()/dotdash_Final_Why_do_MBS_mortgage-backed_securities_still_exist_if_they_created_so_much_trouble_in_2008_Apr_2020-01-fb17668872fd483781eef521a1ddbde8.jpg)

In turn their prices tend to decrease at an increasing rate when rates are rising.

Mortgage backed securities default rate. Figure 1 valuation of mortgage backed securities. Prepaid principal usually variable depending on the actions of homeowners as governed by prevailing interest rates collateralized mortgage obligations cmos cmos are repackaged pass through mortgage backed securities with the cash flows directed in a prioritized order based on the structure of the bond. The overall default rate with mortgage backed securities overall has leapt from 1 46 in may to 3 59 in june the greatest one month increase since fitch started tracking these things 16 years ago which includes the period called the great recession when they collapsed. However mortgage backed securities prices tend to increase at a decreasing rate when bond rates are falling.

An annualized rate of default on a group of mortgages typically within a collateralized product such as a mortgage backed security mbs. Below is a review of the three assumptions that have to be modeled for the mortgage backed securities valuation model. A form of securitization whereby single family residential mortgages are swapped for mortgage backed securities issued by government agencies such as fannie mae and freddie. On the interest rate modeling side there are two primary families of models.

Our mbs market data page allows you to select and display prices in two formats. Basis points selected by default if you select basis points prices are displayed in 0 01 increments. Constant default rate cdr. Investors got hit hard as well as the value of the mortgage backed securities they were investing in tumbled.

Mortgage backed securities are subject to many of the same risks as those of most fixed income securities such as interest rate credit liquidity reinvestment inflation or purchasing power default and market and event risk. This is known as negative convexity and is one reason why mbss offer higher yields than u s. The constant default rate.

When The Qe Music Stops Us Mbs Will Still Be Dancing Investors Corner

U S Mortgage Delinquency Rate 2000 2018 Statista

Rem 2008 Repeat Risks Growing In U S Mortgage Market Bats Rem Seeking Alpha

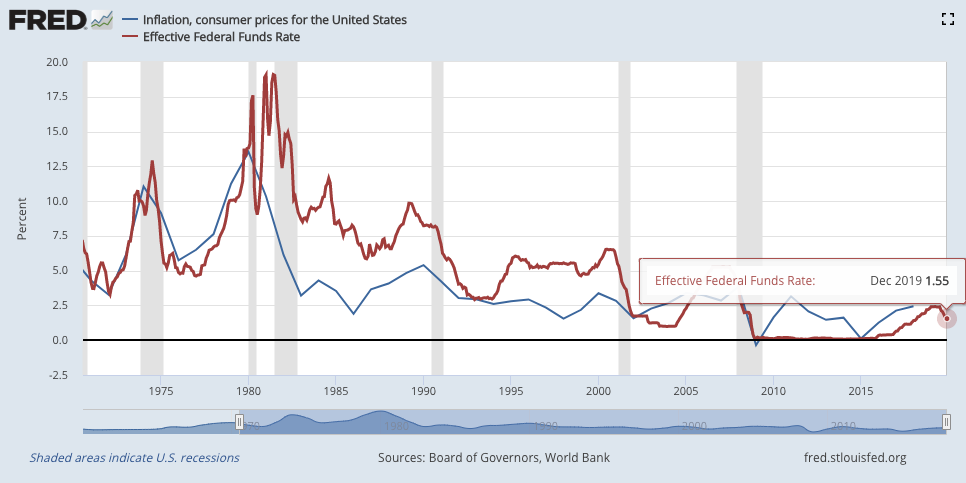

Treasury And Agency Securities Mortgage Backed Securities Mbs All Commercial Banks Tmbacbw027nbog Fred St Louis Fed

What Really Caused The Great Recession Institute For Research On Labor And Employment

Global Structured Finance 2019 Securitization Energized With 1 T In Volume S P Global

Why Do Mbs Mortgage Backed Securities Still Exist If They Created So Much Trouble In 2008

4 Gross Issuance Of Non Gse Subprime Mortgage Backed Securities Download Scientific Diagram

New Challenges For Non Agency Rmbs In 2020 Penn Mutual Asset Management

Covid 19 Almost Broke The Bond Market Then The Fed Stepped In

Reverse Mortgage Investment Trust Inc

Https Www Csbs Org Ginnie Mae Issuer Relief Overview And Outlook Pass Through Assistance Program Ptap

Consumer Abs Under Coronavirus In The Us And China Msci

3 Default Rates On Subprime Mortgages Download Scientific Diagram

Overall Cmbs Delinquencies Decline Hospitality And Retail Remain Elevated

Securitization Mortgage Backed Securities Collateralized Debt Obligations And Credit Default Swaps Credit Default Swap Mortgage Loans Mortgage

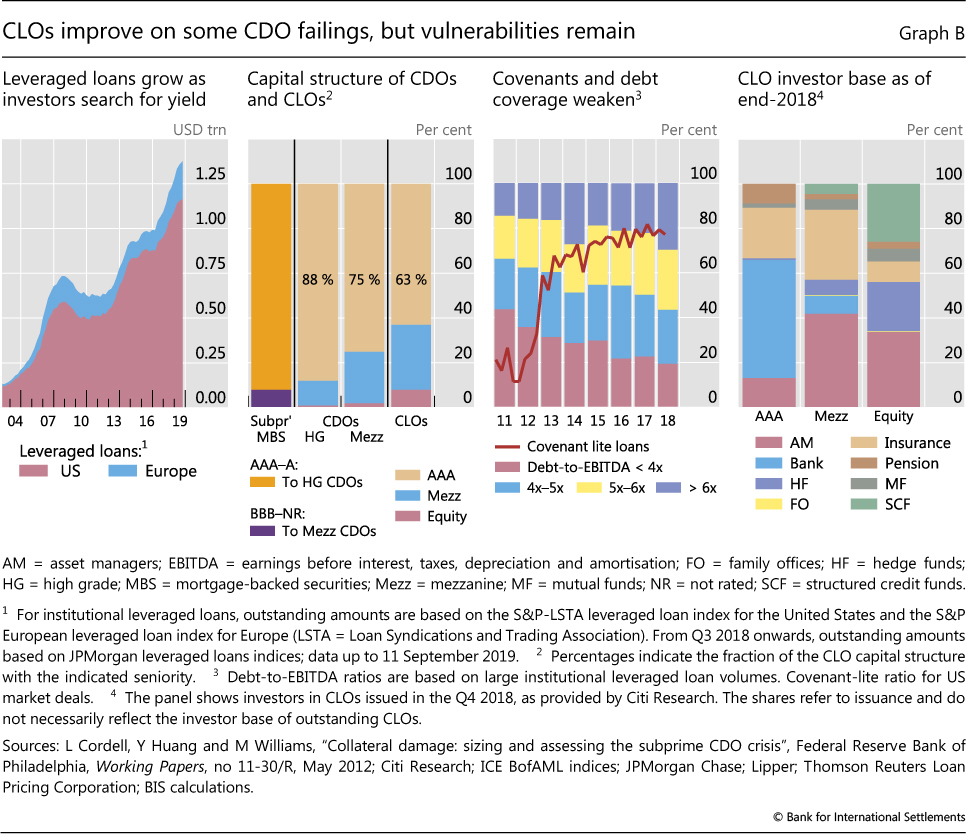

Structured Finance Then And Now A Comparison Of Cdos And Clos

Dtkupj Oucxsdm

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcriwj5pyjmnyqz1xyuvwkm4n Zy3nktubbhiw6ngcylix7upues Usqp Cau

Commercial Mortgage Backed Securities Defaults Spiking

Pdf Estimating Default Probabilities Implicit In Commercial Mortgage Backed Securities Cmbs

Mbs Mortgage Backed Securities Definition Example Investinganswers

Mortgage Backed Securities Ppt Video Online Download

How Mortgage Rates Move When The Federal Reserve Meets Mortgage Rates Mortgage News And Strategy The Mortgage Reports

Mortgage Backed Security Mbs Definition

Mortgage Backed Securities Iii Video Khan Academy

The Handbook Of Commercial Mortgage Backed Securities 2nd Edition Fabozzi Frank J Jacob David P 9781883249496 Amazon Com Books

A Key Metrics Rundown For Securitized Product Investors Breckinridge Capital Advisors

Https Www Newyorkfed Org Medialibrary Media Banking International 09 30 2015 Mbs 10 30am Pdf

/GettyImages-472566664-c8b2a74ab9cb482d89f6623cdeaa51ac.jpg)

Profit From Mortgage Debt With Mbs

Mbs What Are Mortgage Backed Securities Quicken Loans

Mortgage Backed Securities Time To Let Them Off The Naughty Step

Asset Backed Securities An Overview Sciencedirect Topics

Mbs What Really Determines Your Mortgage Rates Mortgage Rates Mortgage News And Strategy The Mortgage Reports

Checking In On Condo Delinquency Rates Dsnews

Covid 19 Is Testing The Resilience Of Global Structured Finance S P Global Ratings

L60htl Gcxd Dm

Repurchase Agreements Mortgage Backed Securities Purchased By The Federal Reserve In The Temporary Open Market Operations Rpmbsd Fred St Louis Fed

Are Dark Clouds Ahead For Commercial Mortgage Backed Securities

Pdf Green Buildings In Commercial Mortgage Backed Securities The Effects Of Leed And Energy Star Certification On Default Risk And Loan Terms

Asset Backed Security Abs Definition